The Evolution of Payment Systems: From Cash to Crypto

Posted on December 5, 2021

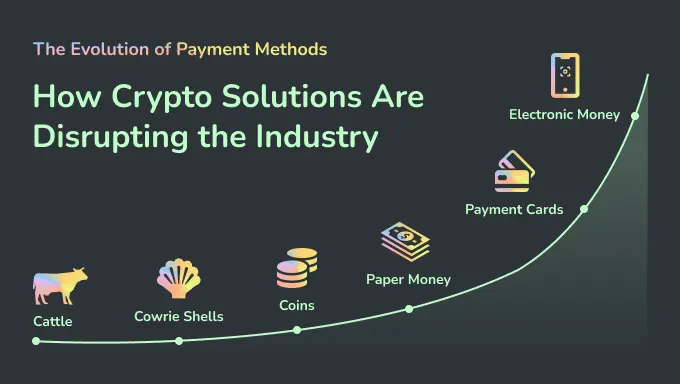

Over the centuries, payment systems have evolved from bartering goods and services to today’s digital currencies. The journey from cash to crypto illustrates the shift from tangible to intangible assets, emphasizing convenience, speed, and security in financial transactions. Here’s an in-depth look at this fascinating evolution:

1. The Beginnings: Barter System and the Emergence of Cash

- Barter System: Before money, trade was based on the barter system, where goods and services were exchanged directly. However, this system had limitations, particularly with matching needs (double coincidence of wants) and measuring the value of various items.

- Introduction of Coins and Cash: Around 600 B.C., the first coins were created in Lydia (now part of Turkey), made of a mixture of gold and silver. Paper money followed in the Tang Dynasty in China, around the 7th century, gaining popularity due to its portability and ease of storage.

2. Modern Banking and the Emergence of Checks

- Early Banking: As trade expanded globally, merchants needed a secure way to store and transfer wealth. This led to the rise of early banking systems. Banks provided safety and enabled the issuance of promissory notes, which would eventually lead to checks.

- The Check System: Checks allowed people to make large payments without handling cash. While this system provided more convenience and security, it still required a manual, time-consuming process and was prone to fraud.

3. The Age of Plastic: Credit and Debit Cards

- Introduction of Credit Cards: In the 1950s, credit cards emerged as a new payment solution, pioneered by Diners Club and later expanded by companies like Visa and Mastercard. Credit cards allowed consumers to borrow money for purchases, repayable over time.

- Debit Cards: Following credit cards, debit cards were introduced, linked directly to consumers’ bank accounts. Debit cards gained popularity due to their convenience, security, and avoidance of debt, making cashless transactions commonplace.

4. The Advent of Digital Payments and Online Banking

- Online Banking: In the 1990s, the internet’s expansion led to online banking, where consumers could manage accounts, transfer money, and pay bills from home. This brought convenience but also introduced new risks, such as phishing and hacking.

- Digital Wallets and Mobile Payments: Platforms like PayPal, Venmo, and later, mobile wallets like Apple Pay and Google Wallet, made digital payments even simpler and more accessible. By storing card information securely, these wallets allowed fast and contactless transactions. In some cases, mobile numbers alone could initiate transactions.

5. Cryptocurrency and Blockchain Technology

- Introduction of Bitcoin: In 2009, Bitcoin introduced a revolutionary concept: decentralized digital currency. Bitcoin transactions do not rely on a central bank but are verified through blockchain technology, which offers a transparent and immutable ledger.

- Rise of Altcoins and Smart Contracts: Following Bitcoin’s success, numerous other cryptocurrencies (like Ethereum, Litecoin, and Ripple) emerged, each with unique features. Ethereum introduced smart contracts, enabling decentralized applications (DApps) and creating a foundation for decentralized finance (DeFi).

- Stablecoins and Central Bank Digital Currencies (CBDCs): While cryptocurrencies are volatile, stablecoins (like Tether and USD Coin) are pegged to stable assets, offering the benefits of crypto without the extreme price swings. Many central banks, including those in China, the EU, and the U.S., are exploring or launching Central Bank Digital Currencies (CBDCs) to modernize the monetary system.

6. Challenges and the Future of Payments

- Security and Privacy: With every innovation, there are security concerns. Cryptocurrencies, for instance, require robust cybersecurity measures due to vulnerabilities in digital wallets and exchanges.

- Regulation and Adoption: Governments worldwide are actively debating the best ways to regulate crypto to protect consumers without stifling innovation. The acceptance of crypto for day-to-day transactions remains limited, but large institutions and some governments are beginning to adopt it.

- Blockchain Beyond Payments: Blockchain technology’s use extends beyond just crypto. It’s being tested in various industries, including supply chain management, voting systems, and digital identities, due to its ability to provide transparency and reduce fraud.

Conclusion: The Road Ahead

The evolution from cash to crypto is part of a larger trend toward digitization, aiming to make payments faster, safer, and more accessible. As technology advances, the future of payment systems will likely blend both traditional and new methods. Payment platforms will become more seamless, providing instant, borderless, and secure transactions for individuals and businesses alike.

Cryptocurrencies and blockchain technology have brought transformative changes, but we are only at the beginning of a new era. As cash loses its dominance, digital and decentralized currencies may define the future, moving us closer to a world where physical money becomes obsolete. However, these changes will require global cooperation, regulatory clarity, and innovative technology to ensure they are secure, accessible, and beneficial for all.

Categories: Banking